Continuing last editions list of most read articles. Sharing Top 15 Most Read Articles of 2019 read on my weekly newsletter “Best of the Web”.

Most Read Articles: 15) PG’s awesome essay on ‘What makes a genius’ 14) How can a non-tech guy become the go-to advisor to some of the world’s most powerful tech companies? Great profile of a fascinating person, Bill Campbell – The Secret Coach. 13) The Gross Margin Problem: Lessons for Tech-Enabled Startups. Read here 12) Hanlon’s Razor (and why people are nicer than you think). Read here. 11) How India’s Growth Bubble Fizzled Out. Read here 10) Morgan Housel’s post, ‘Betting on things that never change‘ 9) Beautiful essay by Paul Graham on what it means to have kids. Read here 8) A light breezy read on “Rich People’s Problems”. Read here 7) How to build optionality into your life. Read here 6) Peter Thiel’s Contrarian Strategy. Read here 5) Capital ROI of various Indian Startups. Read here 4) Tiny networking tip by Ben Horowitz. Read ‘Strike when the Iron is hot‘ 3) Paul Graham’s classic 2004 essay, ‘How to make Wealth‘ 2) Maria Montessori and 10 famous graduates from her schools. Read here 1) My new goal in life is to avoid a mid-life crisis. Read here

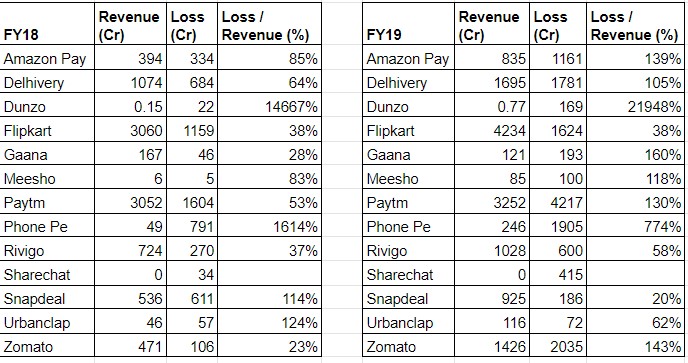

While Uber & Lyft’s abysmal IPO sustained the push to margins and profitability, explosion of WeWork was the final nail on the coffin.

Since the relatively nascent Indian startup ecosystem is a reflection of US & China (in some aspects), one can expect to see a stronger push for Margins/Profitability in India as well.

I tried to collate a view from all publicly available data on revenue and losses for various Indian Startups to get a view of what’s happening. Hope you’ll find it useful too.

Source: Paper VC, Entracker, Mint, ET etc

As more Indian Startups file their earnings for Financial Year 2019, more data will emerge. I’ll try to update this view.

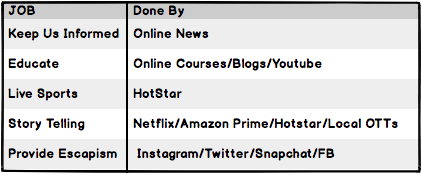

In a 2013 piece, Ben Thompson outlined the following ‘Jobs TV Does’

Keep us informed

Educate

Give a live view of sporting events

Enlighten and story-tell

Provide escapism

Subsequently he makes a call for “Unbundling of TV” whereby a different category/product will come about offering a better way to get each of the above mentioned jobs done.

Thing started changing well before Ben wrote that piece and some of those changes seem solidified, at least for now.

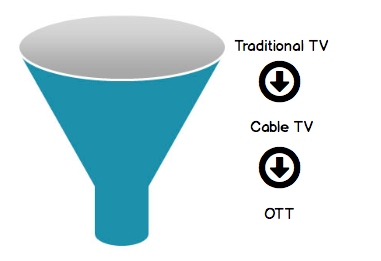

TV Unbundling In India, 2018

Migration from TV to OTT

As per a recent survey by BARC India, 197 Mn homes in India have TV with a total TV penetration of 66%. The survey also shares that over 835 Mn individuals have access to TV. The advertising spend for the medium estimated to be Rs 31,596 Cr ($4.5 Billion).

While TV is enjoying it’s last phase of penetration growth (like print media) there is a big migration from TV underway in India with Gen-Z & Millennials leading the wave.

The first phase saw a move from ‘Traditional TV’ to ‘Cable TV’ with a huge portion of country installing set top boxes to get access to niche programming, round the clock at a reasonable price. The second phase is seeing the move from ‘Cable TV’ to ‘OTT/On-Demand Video’.

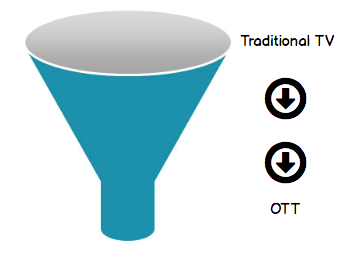

Journey from Traditional TV to OTT

I believe currently this transition is at play with users gradually moving from one stage of the funnel to the next. However, over the next few years most users will skip the set-top box stage and jump straight from TV to OTT platforms.

People will Skip ‘Set-Top Box’ and jump straight to OTT

OTT is High Growth Market

India has been a huge market for Films, TV Shows and Sports. Increasing high-speed internet penetration, falling data prices, entry of big players with huge budgets along with original content aimed (mostly) at youth has over the years set the ball rolling for OTT (Over-The-Top) consumption in India.

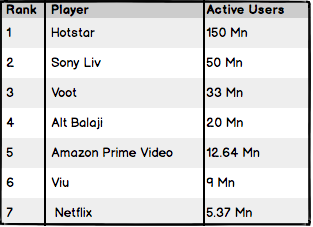

The current Indian streaming market is roughly pegged at $300 million with 30 OTT players with Hotstar being the most popular service.

Top OTT Players in India (source: impactonnet.com)

As of today, OTT is one of the hottest markets in India with everyone scrambling to get a piece of the pie. OTT viewers are growing by 35% Y-O-Y and projected to grow to 355 Mn by 2020. OTT video revenue is expected to reach Rs 5,595 Cr (~$800Mn) by 2022. With projections like these the current gold rush starts to make sense.

OTT Market Players:

With over three dozen players, OTT is becoming a crowded market with players trying to attack it from all sides. From small digital content studios to giant media/production houses, everyone’s got their eyes on the prize.

The types of players can be divided into the following categories

Media Groups ( Star, Sony, Zee etc)

Production Houses (Eros, Balaji Telefilms etc)

OTT Platforms, International & Local (Netflix, Viu etc)

Internet Companies (Amazon etc)

Digital Content Platforms/Studios (Arre etc)

Others (Aditya Birla Group etc)

A fast growth market with a lot of headroom to grow, voila. However, similar to what I mentioned in ‘The Transportation Layer Protocol of Business‘, while everyone is free to compete, not everyone stands a fair chance at winning. Moreover, even if one is able to create value, in absence of a sound business model, they just might be not to capture it.

Will come back to explore this topic in a later post

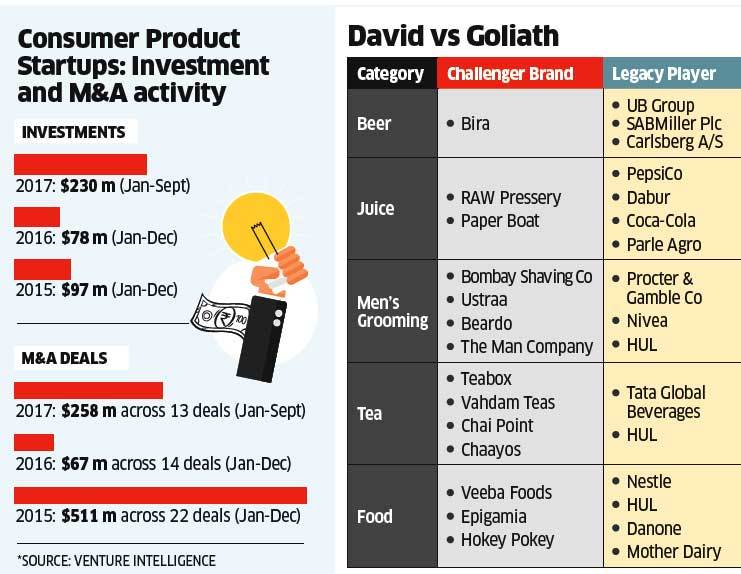

Over the past 5 years or so, consumer product startups have been slowly but steadily picking pace in India. While their scale might be significantly low in comparison with e-commerce, ride-sharing or food delivery startups, their seems to be a lot of action in the space.

India’s FMCG market is pegged to be around $185Bn. Traditionally, the large players in FMCG/CPG space have operated by owning a massive distribution pipe (Wholesalers, Distributors & Retailer), doing massively expensive marketing campaigns and selling commoditised products. All of this is starting to change.

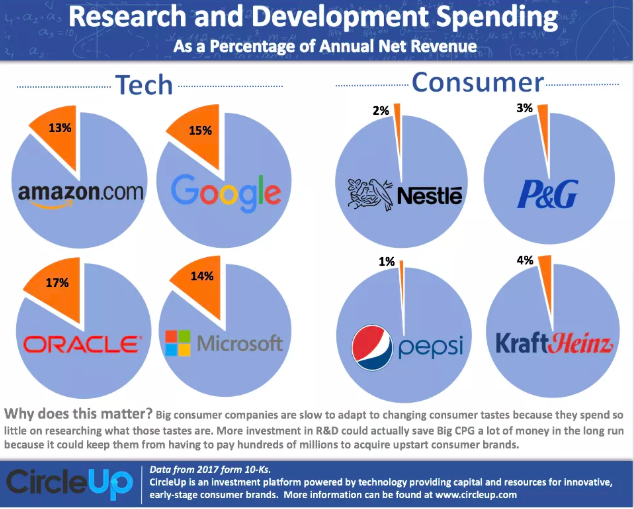

That smaller startups are trying to disrupt incumbents extended to FMCG category is a natural after effect of the internet penetration and the subsequent second-order effects. Also, as shown below, the CPG brands globally are infamous for their lack of innovation.

R&D Spending in Consumer Goods Cos as compared to Tech Cos

Factors that favour growth of FMCG startups: Include changes in status quo for:

Innovation

Production

Marketing

Distribution

Given the rising discretionary spends and ability for internet to help micro target, upstart startups can now decide to make products not for a mass segment but for niche consumers subset. For ex: Instead of making Real or Tropicana Juices aimed at all and sundry, there can now be Raw Pressery or Paper Boat aimed at premium/niche segment of the market.

Since the target segment is a smaller niche, it fundamentally changes how companies approach Production, Marketing and Distribution.

Innovation (Loved by a few vs liked by a lot): Given a niche customer segment, a startup can focus on making a great product that their customers will really love over a good/slightly better than average product that a lot of people will be fine using.

Production (Lower Upfront Fixed Cost Requirements): Unlike earlier times, a startup can now think of starting small and launching few niche products with a reasonable manufacturing setup and invest in production as they grow.

Marketing (Lower Variable Costs): A startup these days can get the wheels of marketing rolling but starting with ads on Google, Facebook, Instagram and others with a much smaller budget. Another aspect of marketing is the solid brand proposition that most niche CPG startups are able to drive due to their innovative offering.

Distribution (Lower Upfront Fixed, and Variable Costs): Compared to earlier times of building a comprehensive retail supply chain across the state/country to store and deliver goods, a startup can get started with minimal inventory and deliver products directly to consumer (D2C) through their website/3rd party marketplaces and scale distribution spends as their traction grows.

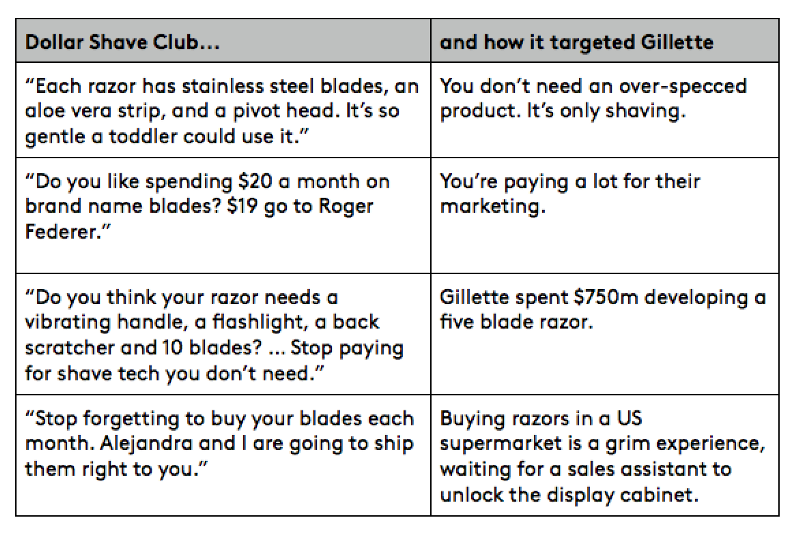

Source: Dollar Shave Club/ Kantar Futures

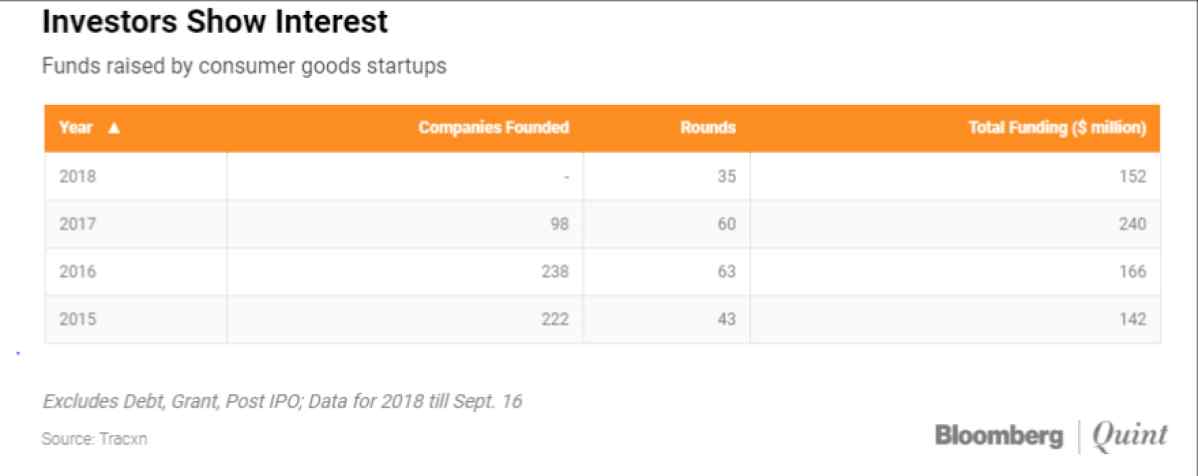

VC activity in the space has been on rise with some focussed funds like DSG actively investing in startups. DSG has around a dozen investments in India including Chai Point and Raw Pressery. Consumer Goods startups have raised over $152 mn in 2018 (so far).

via Bloomberg Quint

via Economic Times

via Economic Times

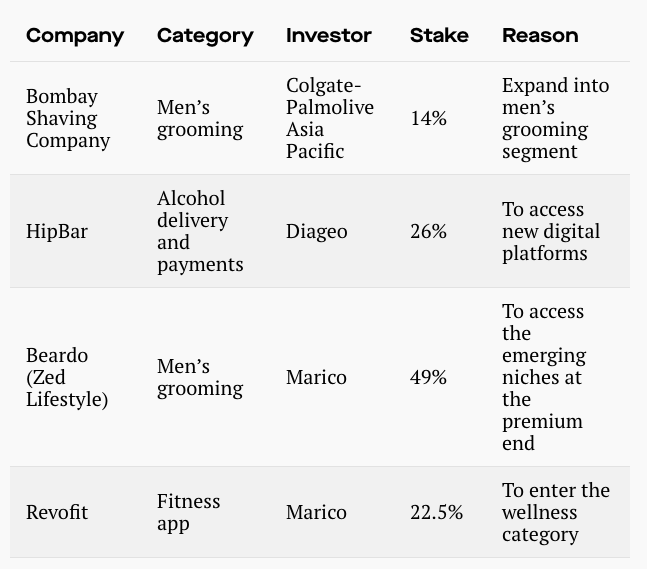

The Bigger brands have also started making their moves in Indian Consumer Goods Startups.

Some other players that attracted investments from bigger players Happily Unmarried’s Ustra (Wipro Consumer Care) and Forest Essentials (Estée Lauder). The biggest player in the D2C category (not FMCG really) that has done exceedingly well in Lenskart.

With increasing GDP per capita, better penetration of high-speed internet, increasing transition towards e-commerce fuelled by significant VC funding and some M&A activity, the FMCG space is bound to grow and thrive. It’d be interesting to observe how various startups evolve and make great businesses.

On closing note, here’s the great introductory video by DollarShaveClub that set the ball rolling.

For a while, I’ve been thinking about a lens or a mental model to look at the opportunities possible while once a user is in a ride-sharing vehicle.

Given that millions are using ride-sharing services like Uber and Ola everyday to commute and that they are slightly better suited to being offered another product or service during their commute makes them apt for some interesting possibilities.

Let’s divide the commute into different segments based on distance covered.

1. Short – Cabs, Bikes, Bicycles 2. Medium – Cabs, Bikes 3. Long – Cabs, Bus

Out of the commute options above, a couple make for a good fit to be ripe for some add-on opportunities. The contenders include

1. Cabs – Medium & Long Distance 2. Bus – Long Distance

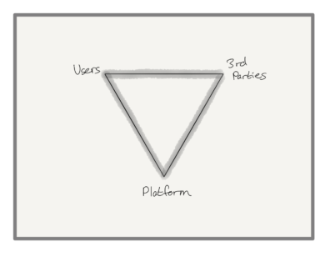

When you think of a platform, the following image comes to mind

The underlying structure comprises of:

1. Users using a platform frequently. 2. Platform allowing 3rd parties (developers/companies etc) to offer products that users can access. 3. Platform collecting rent for offering 3rd parties a connection to users.

Food Outlets in Delhi Metro Stations

Delhi Metro has had food outlets in its metro stations for a long time. Apart from Advertising on the metro train itself, this is one of the biggest sources of revenue from them.

Unlike iOS/Android app stores where anyone can freely publish an app (subject to certain T&C), with it being a physical play one can’t just set up a shop on a metro station. In that sense, one can think of it as a ‘Managed or Curated Platform’. While anyone can apply for a shop via a Tender, the number of shops is constrained and can’t ever be as long tail as in the digital world.

Keeping the limitations of atoms aside and the fact that most of these commute services are structurally aggregators (Ola/Uber have homogeneous supply, decide which cab to be dispatched and more), thinking about the ‘Commute vehicle’ as a platform lets one imagine various possibilities. Let’s take a look at some options

Advertising (Brand and Transaction Driven)

Commerce (Physical and Digital)

Entertainment (Audio, Video, Games)

Advertising (Brand and Transaction Driven): This one is classic, using the platform for un-targeted/blanket brand campaigns or using the platform for targeted ads what could drive the user to a transaction.

For ex: Sharing a promo code that enables a special discount to try a new app. (QR codes?)

I feel there could be an interesting play to build a way to deliver targeted campaigns to users. Given the low scale, smaller/upcoming brands might find it more useful.

Cab Branding for Mobikwik

2. Commerce (Physical and Digital):

This is particularly interesting and under-explored (except for food joints in metro stations etc). Our impulse purchase behaviour, coupled with internet connectivity, convenience and instant gratification makes it powerful.

A few months back Uber tied up with Cargo to enable riders to buy snacks and confectionery. Apparently, Cargo helped drivers earn more than $100 extra per month and has shared over $1mn with its drivers since its launch

Snack Ordering Via Cargo

In terms of fitment, the light snacks and confectionery seems to be a great fit. Want a coke on your ride back from Airport or want to grab a quick chocolate on the evening ride back home? All seems, possible.

Apart from the food stuff, can the vehicle enable you to buy some digital stuff or physical stuff digitally? Could be the boring stuff that one doesn’t get time/wants to do during core hours

a) Ordering food or grocery while I’m on the way to home. But then one might use mobile apps they already have on their phone, in which case the advertising can act as a nudge to make user transact on their phone itself .

“Don’t feel like eating home food? Order your favourite cousin and have it delivered within 10 minutes of you reaching home (and get 10% off)”

b) Gifting, Getting Utility/Services work done could be some possibilities

3. Entertainment (Audio, Video, Games):

This is another natural fit for a commuter. Passengers (and riders) have been listening to music, watching videos etc since forever and offering an extension of the same to the user while commuting is perfect.

Bhavish Announcing Launch of Ola Play

While, I’ve never used the other features (like car control and stuff) I can safely say, Ola Play launched in Nov 2016 is a great and useful innovation.

I’m not too sure on the current model for Ola Play but given its relevance for users and the good execution (network connectivity, hardware, ux etc) it can be a great way to offer more value to the customers.

Some possibilities around Live Streaming Events, Live Gaming, Podcasts, Trial Subscriptions for OTT, Short Length Media, Original Content etc would be very interesting to explore.

There could be potentially a few more options { in-cab feet/back massage machines?:) } to leverage the 30mins-60mins+ commute time, internet connectivity, fewer distractions, other needs (hunger, killing time etc).

It’d be interesting to see how various companies evolve their offerings in this space, would the ride-sharing companies act as an aggregator or have a platform play and which of them turn out to be well executed, scalable and profitable.

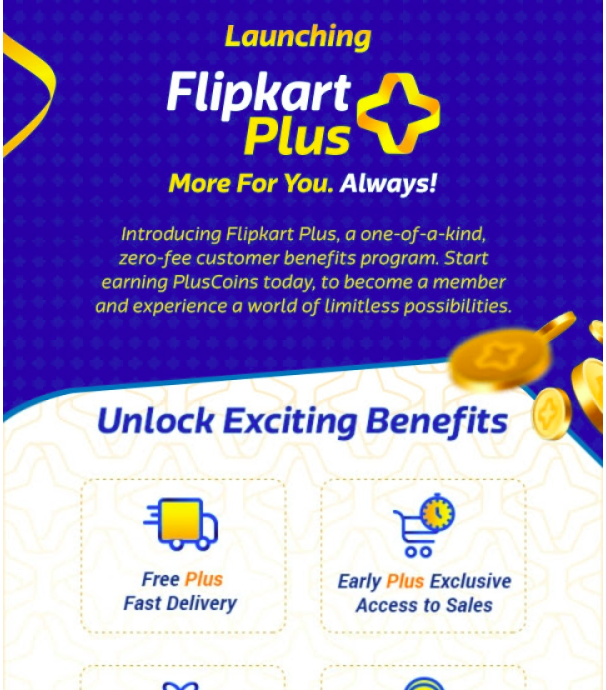

Flipkart, the country’s biggest e-commerce company announced the launch of their loyalty program or customer benefits program (as they are calling it) on India’s Independence Day .

Launch Emailer

Here’s a quick summary of the program

Opt-in membership with zero fee

Free Expedited Shipping

Exclusive access to promotional offers on Flipkart

Reward points (coins) for purchases on Flipkart, which can be redeemed to buy offers on & off Flipkart (other vendors like Bookmyshow, Cafe Coffee Day)

Superior & Priority Customer Support

Membership is just a click away

Flipkart Plus Landing Page

For an e-commerce company to become a sustainable business at scale, customer loyalty (aka retention) is a must. With increased competition and massive customer base, retention is the most obvious and un-avoidable path for all sizeable e-commerce companies, thus the recent public push towards launching loyalty programs.

Coming back to Flipkart, Flipkart Plus is their second attempt to launch a loyalty program. The first attempt was made in 2014.

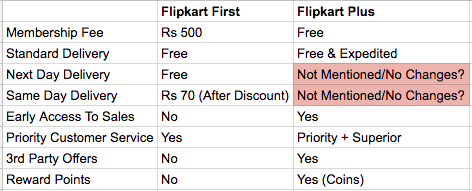

Flipkart First (Launched in 2014)

‘Flipkart First’, ran for 2-3 years before the company quietly setting the sun on it. Since I was an active customer back then, I purchased ‘Flipkart First’ membership twice to avail the benefits.

Here’s a quick overview of how the two programs compare with each other

Flipkart First Vs Flipkart Plus

Summarising the key changes:

1. Waving off Membership Fee 2. No commitment over delivery time and charges 3. Adding early access to exclusive deals 4. Superior and Priority customer service 5. Introducing 3rd part offers and reward points

Let’s try to quickly unpack these changes

Free Memberships: Positives — Increased Uptake Negatives — No additional revenue from membership fee

IMO a loyalty program without membership fee is not reflective of brand power and will always restrict goodness you can provide.

Free and Expedited Delivery: Positives — Increase in both order count (significant) and revenue (insignificant) Negatives — Extra shippings costs.

Since membership is free and so is shipping, essentially users have no incentive to consolidate their orders and thus they can & will choose to place standalone order for low ticket items but will they spend significantly more because of this, I don’t think so.

Early Access To Exclusive Deals (Actually just Exclusive Deals): Positives — Depends on quality of deals. Could lead to more orders & revenue Negatives — The deals on low ticket item products can put further pressure on shipping costs.

The way I see it, I don’t expect great deals for Plus members. Let’s wait and watch on this.

Superior & Priority Customer Service: Positives — Difficult to measure and communicate value to users. Negatives — If some changes are actually done at CRM, process and team levels. The costs for this could be significant.

Unless a customer buys extremely regularly and interacts with CS often they can’t really see the difference. Even if the experience is better, I’d actually prefer to not having to talk to CS at all.

Also, I’d never want customers to feel they are treated unequally. So generally speaking, I don’t like this feature.

3rd Party Offers and Reward Points: Positives — Additional benefit to customers, should bring some additional revenue from 3rd party. Negatives — The offers currently are unpleasantly few and the usage terms are not friendly (to the point of discouraging impulse use).

Giving formulaic reward points for purchases in form of coins could have been good had they allowed people to redeem them while shopping (think Paytm Cash) but in the current form, users can redeem coins to buy offers on 3rd party or Flipkart. First option currently is un-exciting and second one involves fair amount of friction

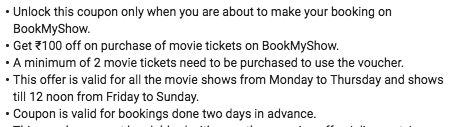

Expect a lot of low ticket orders like theseUnfriendly Terms: Of course I will remember all this two days in advanceRedeeming Rewards: 50 Coin Offers

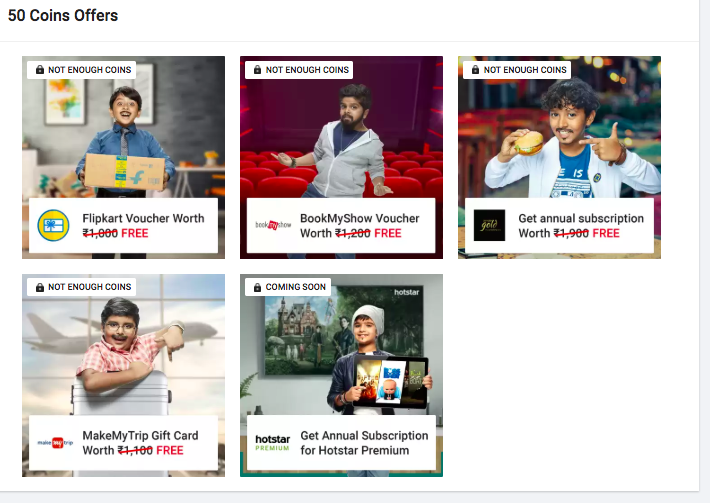

50 Coin Offers

Rs 250 earns you 1 Coin, so you need to spend Rs 12,500 to earn 50 coins. There’s also a catch, you can’t earn more than 10 coins in an order. So in effect, a user need to place multiple orders (5 big orders or 50 small ones) of Rs 250 or more to accumulate 50 coins.

Once a user has spend Rs 12,500 they are eligible for these offers – Rs 1000 worth free Flipkart Voucher (8% cashback) – Rs 1200 worth BMS voucher or Rs 1900 worth Zomato Gold.

These offers are definitely interesting for regular customers as they get all these benefits for free.

Would people spend more often on Flipkart or move to Flipkart because of these benefits (more offers to come) would be interesting to see.

Was reading this great post on Showing Passwords on Log-In Screens by the awesome @lukew and thought of checking how various apps (Indian and Global) that I use are handling their login/sign in page, thus this post. Also, notice which apps use login and which use “sign in”

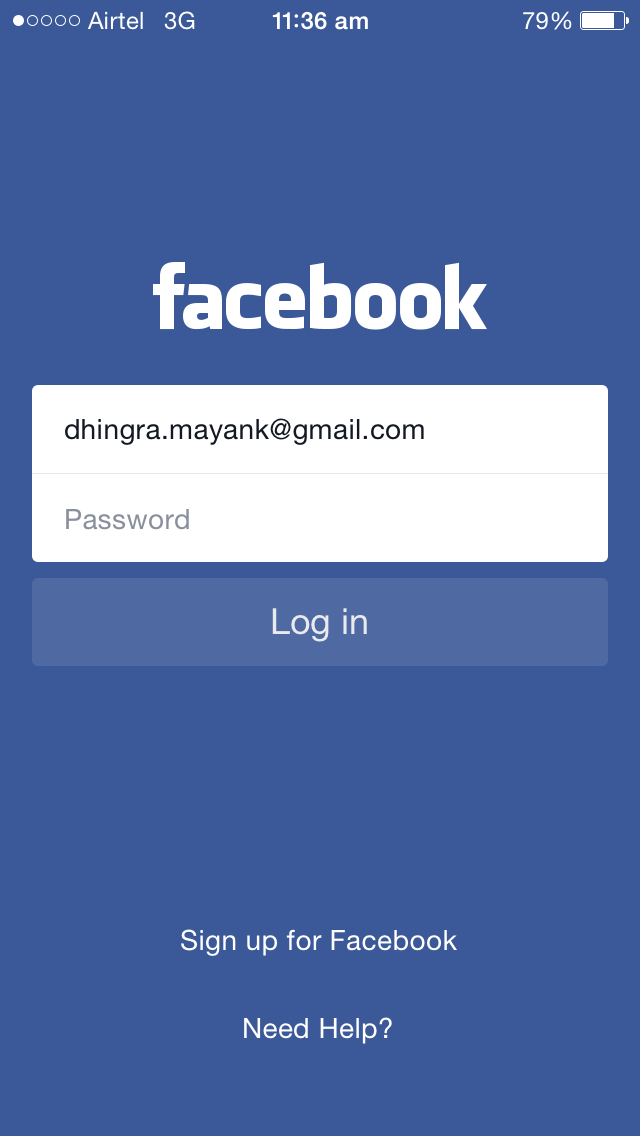

1) Facebook – Log in

Neat, Minimalistic and incredibly simple.

No of buttons on page = 1, No of input fields = 2, No of links = 2

Option to see password – No

Also, notice how they say “Need Help” instead of the typical “Forgot Password” option used by almost everyone

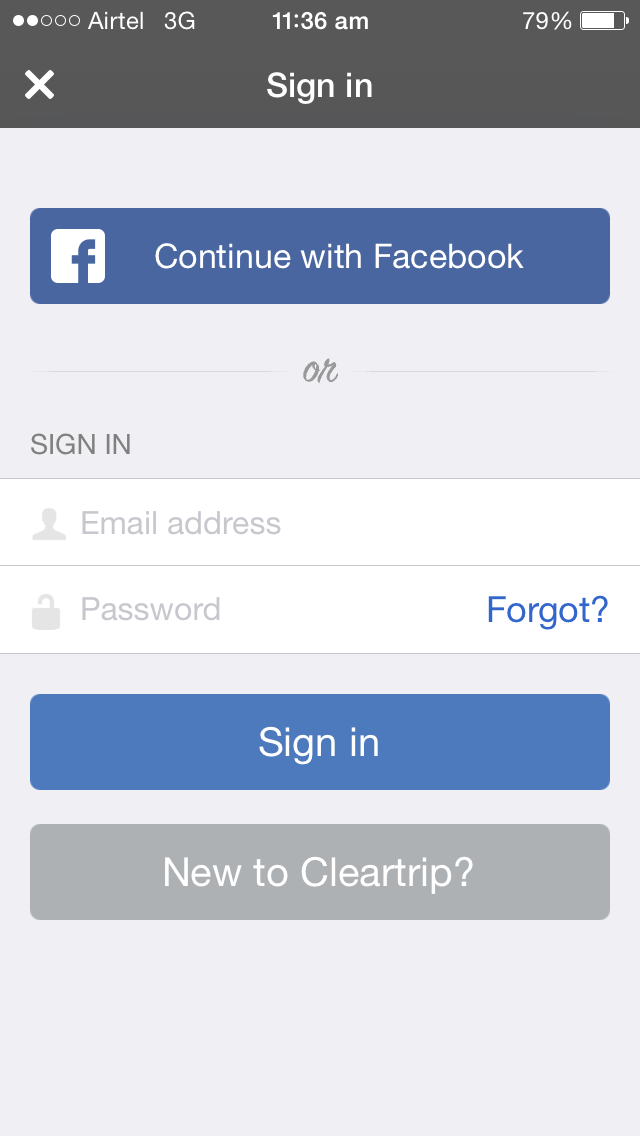

2) Cleartrip – Sign in

A bit cluttered

No of buttons on page = 3, No of input fields = 2, No of links = 1

Social Login Options: 1

“Continue with Facebook”?, that’s a rather different(vague?) copy for a login with Facebook option.

Option to see password: No

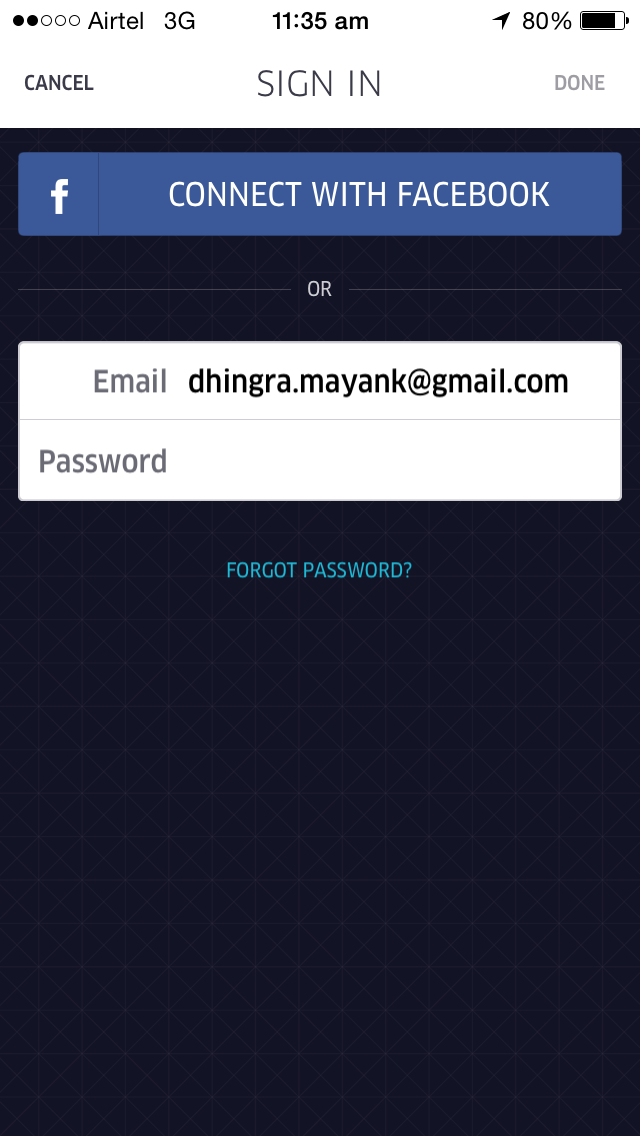

3) Uber – Sign in

With no branding, it’s impossible to guess which app is this.

Minimalistic and Neat

No of buttons on page = 1, No of input fields = 2, No of links = 1

Interestingly they don’t have a button to Login, only an option at top and one of keyboard (Done)

Option to see password: No

Social Login Options: 1

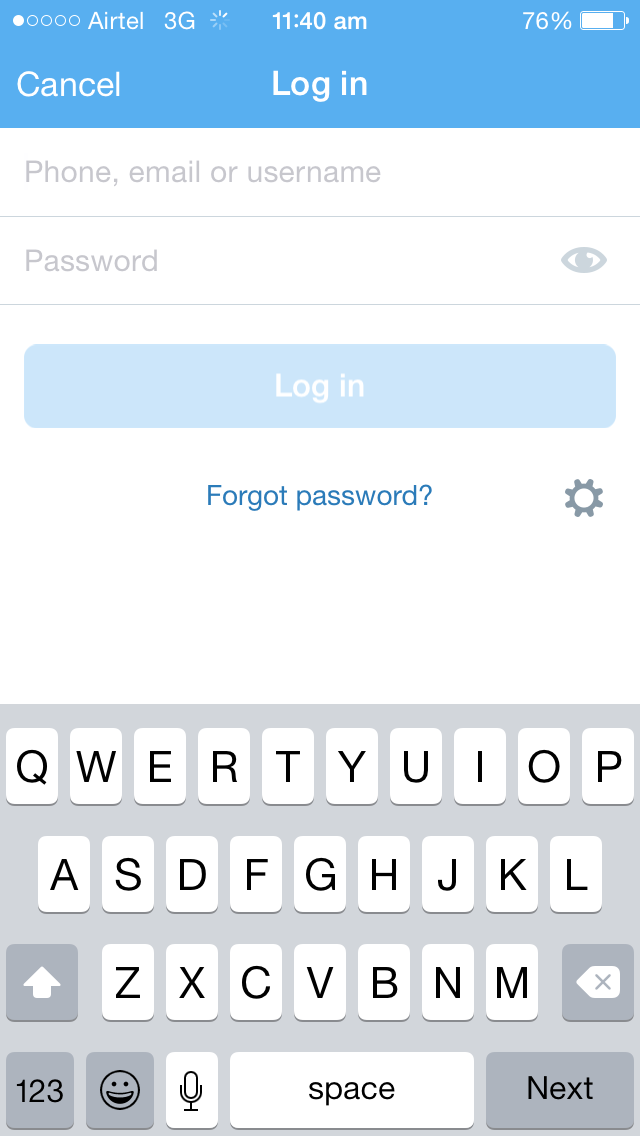

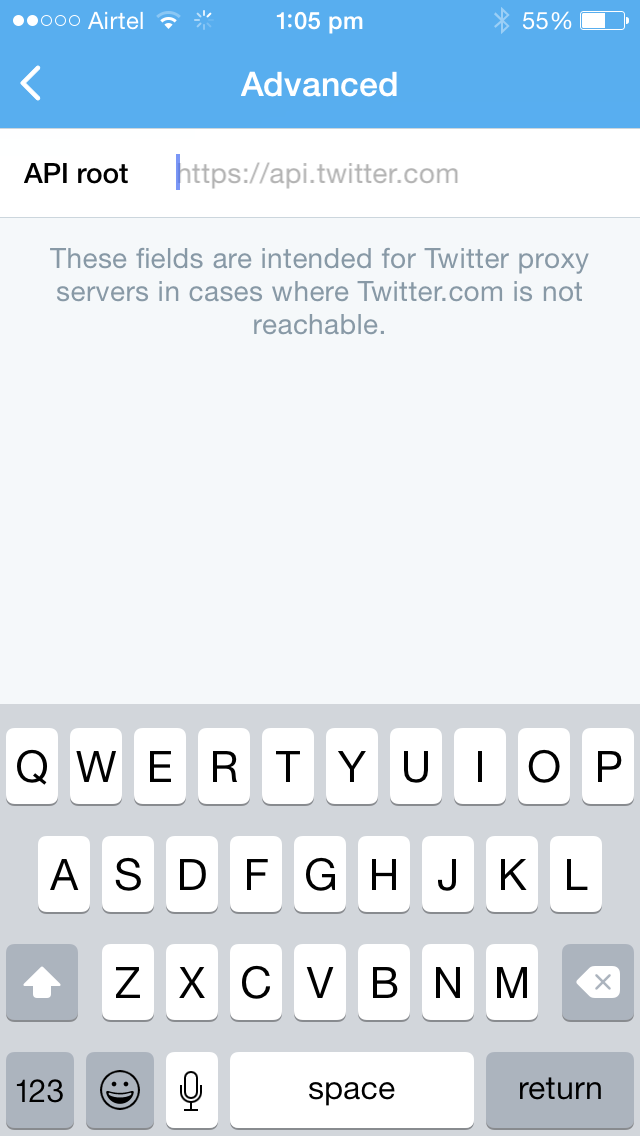

4) Twitter – Log in

Branding: No

Minimalistic and Neat

No of buttons on page = 1, No of input fields = 2, No of links = 1

Option to see password: Yes Very interesting: The setting icon which opens to this

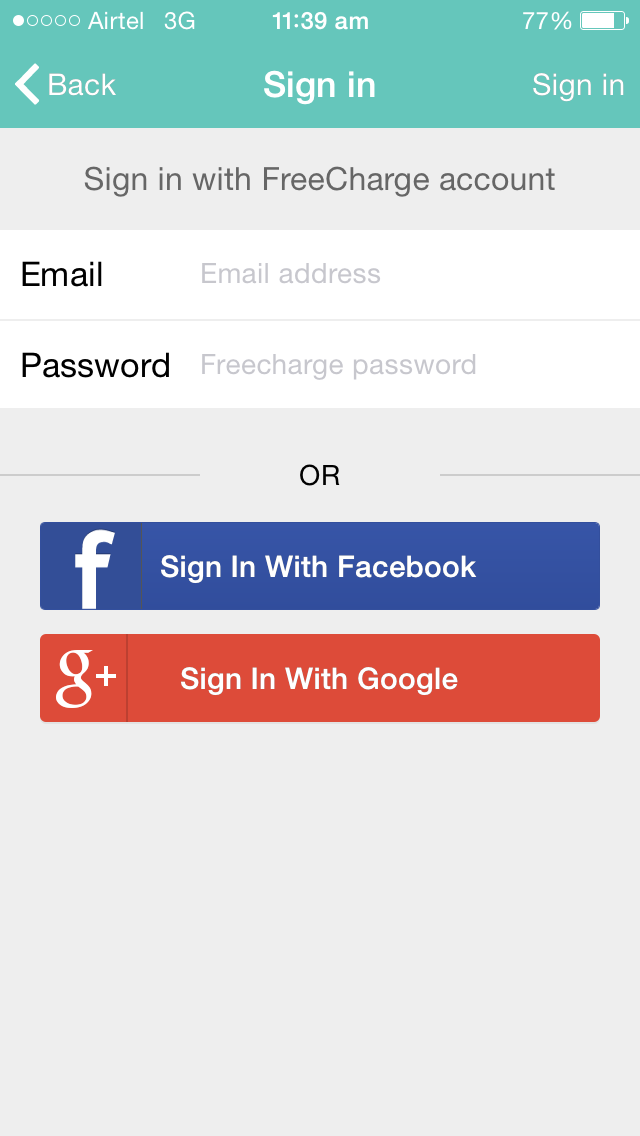

5) Freecharge – Sign in

Branding: Yes

Full of options yet net

No of buttons on page = 2, No of input fields = 2, No of links = 0

User needs to click Sign in on top right or done from keyboard to proceed

Option to see password: No

Social Login Options: 2

Consistency in using “Sign in”

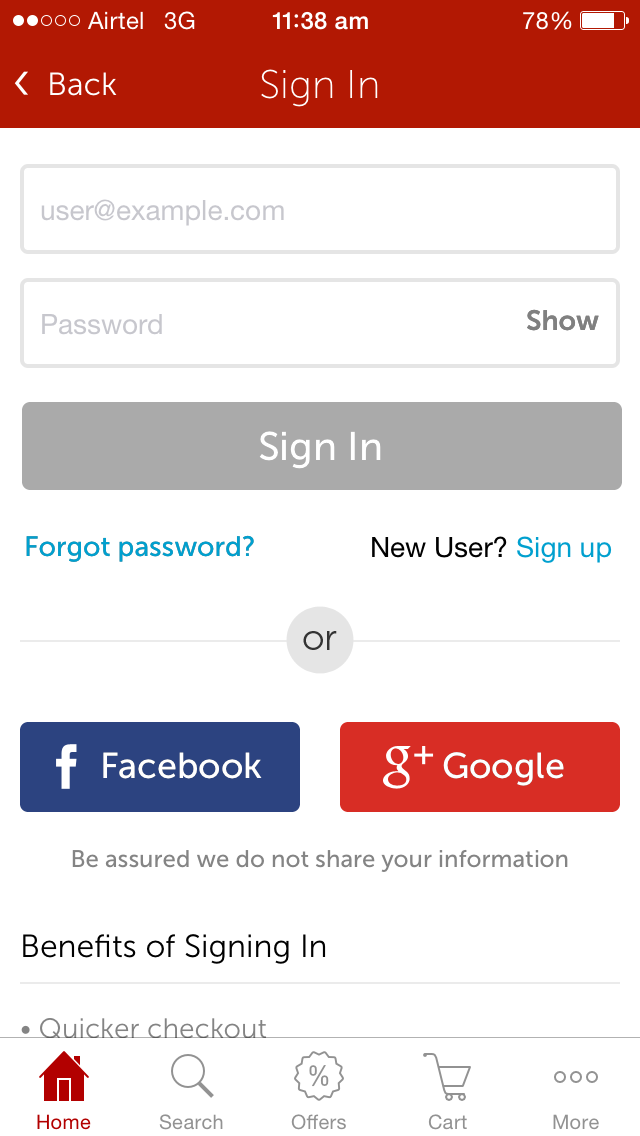

6) Snapdeal – Sign In

Branding: No

Brimming with options to the extent of being cluttered and heavy on the eye.

No of buttons on page = 3, No of input fields = 2, No of links = 2

Option to see password: Yes

Social Login Options: 2

The CTA for social login is just the name of social platform, curious if/how it impacts Clicks

Interesting: The page is in two folds, with second/bottom fold talking about “Benefits of Signing In”.

One wonders, is this bit a carry forward from the old days and nobody in Products team bothered to question the need for this?

Also, the presence of menu on Sign in page is conspicuous

7) Jabong – Login

Branding: No

Multiple options to Login

No of buttons on page = 2, No of input fields = 2, No of links = 2

Option to see password: No

Social Login Options: 2

Interesting: Seems like Jabong prefers their users to Login using social sites over their own account on Jabong.

8) Myntra – Login

Branding: No

No nonsense Login page. Simple and beautiful

No of buttons on page = 1, No of input fields = 2, No of links = 1

Option to see password: Yes

Social Login Options: 0

Though they don’t have an option of social login but I like the simplicity of this page

9) Paytm – Sign in

Branding: Yes

Too much going on here

No of buttons on page = 3, No of input fields = 2, No of links = 3

Option to see password: Yes

Social Login Options: 2

Paytm has T&C links, while no one else does. Also, Paytm is the only app other than Twitter, that let’s you login using your mobile number.

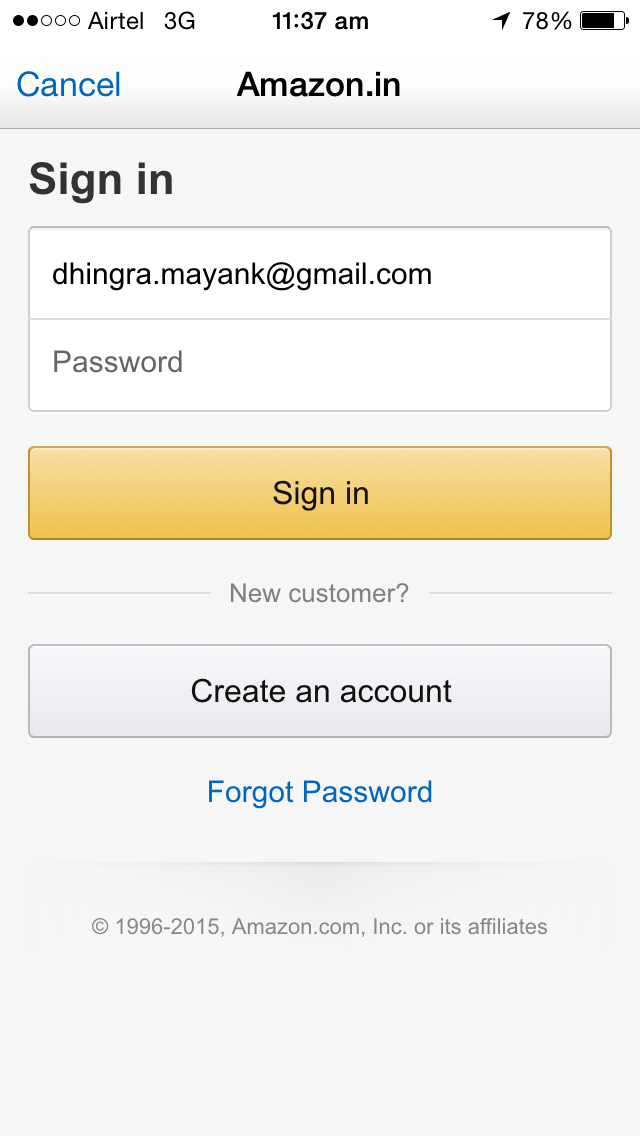

10) Amazon – Sign in

Branding: Yes

Neat and sure

No of buttons on page = 2, No of input fields = 2, No of links = 1

Option to see/hide password: No

Social Login Options: 0

The create an account on Amazon’s login page is very clear and should be helpful to New users who’ve landed at Sign in page

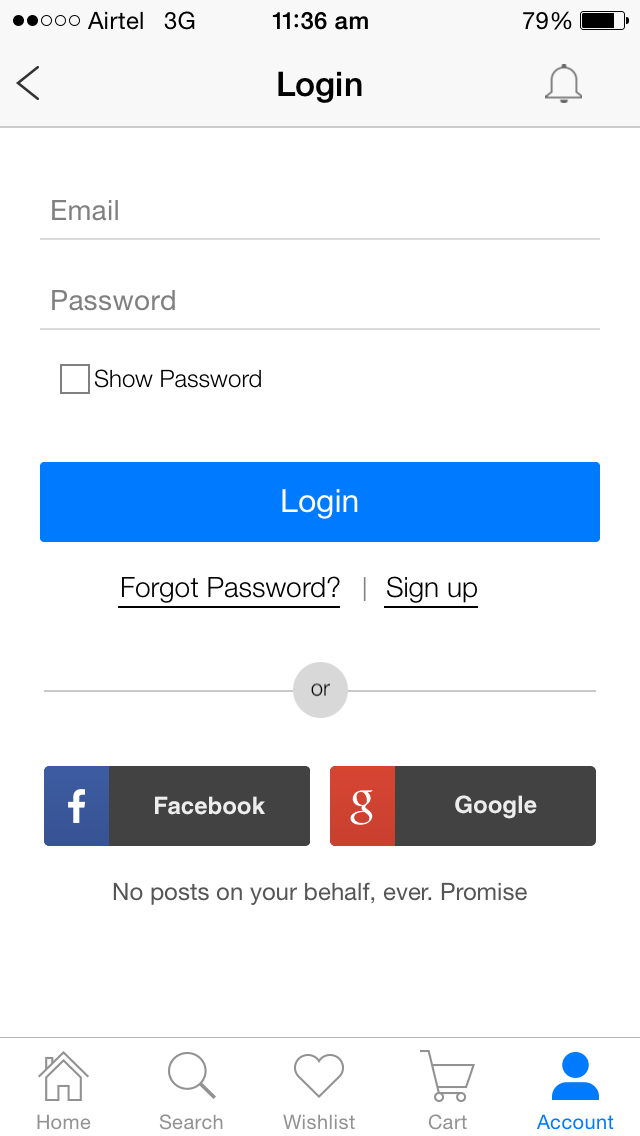

11) Flipkart – Login

Branding: No

Well structured and neat

No of buttons on page = 3, No of input fields = 2, No of links = 2

Option to see/hide password: Yes

Social Login Options: 2

“No posts on your behalf, ever. Promise” should help in increasing the trust and making more folks using Social Login.

Menu on login page is something I am not too sure of being needed/useful. Similarly the notifications icon on top right? In what case would notifications be needed on the login page?

Which Login pages do you like/dislike most from these ?and why?

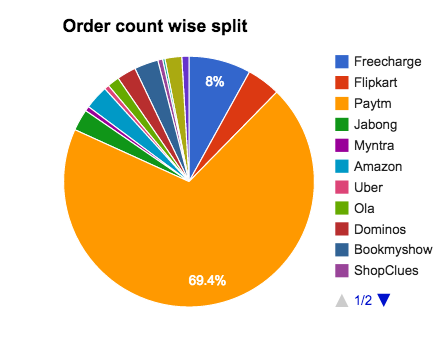

Not surprisingly, I placed the most orders in 2014 on Paytm (close to 70%), followed by Freecharge (8%), Flipkart (4.3%), Amazon & Bookmyshow. Various cashback schemes run on Paytm are the reason behind the skew of order count

Talking about physical goods #1 was Paytm (Aggressive offers early on), followed by Flipkart, Amazon & Jabong

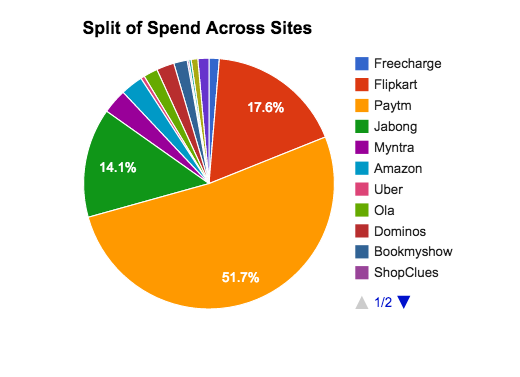

2) Split of spend across sites

The story starts to clear up a bit when we look at split of spend across various sites

While 70% of orders I placed were on Paytm, 52% of the money I spent online went their. Flipkart (17.6%), Jabong (14.1 %) & Myntra (3%) came next. The ticket size for Amazon has been quite less

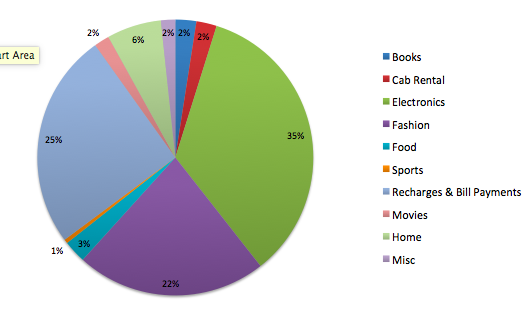

3) Split of spend across categories

This is quite revealing for me. While last year I spend considerable chunk of money (spent online) buying books, this year books formed a very small piece.

35% of money I spent shopping online last year, was spent on buying Electronics (mostly mobiles) & related Accessories. 25% was spent on recharges/bill payments and a significant change towards Fashion with 22% of my spend went there.

Some Interesting Bits: 1) I spent more ordering food online than buying books (Still can’t believe it or Maybe I got better deals at books 😉 )

2) I spent more on Cab rentals than movies ( I don’t take cabs as much) and almost the same amount as I spent ordering food online

3) Between Fashion & Electronics – 57% of my money was spent

Purchase Summary Orders placed: 321

Digital goods (recharges, bill payments and movies): 252

Money Spent: Rs 1,72,448

Money spent on Physical goods: 1,24,621

Closing Thoughts/points 1) I’m not the most savvy online purchaser but I do tend to compare prices before buying stuff and have started using mysmartprice and more recently buyhutke (Chrome plugin)

2) Online mega sales trigger my purchases (super surprised to find out, I ordered on Myntra this GOSF after a break of 1 year from last GOSF). Made purchases on Big Billion Day and even Myntra’s “End of Reason” sale today

3) While I preferred purchasing on desktop (ease of selection, multiple tables, price comparison etc). I’ve started buying stuff straight of mobile. While for many purchases mobile still serves as the initiation point of my purchases and the same happens other way around, I add items to cart on web only to order them later on mobile when free

4) Most of my purchases (especially Fashion) are impulse (discount driven If I can admit), while Electronics etc are kinda planned

5) I’ve jumped the ship completely when it comes to paying by card. Almost, all my purchases (90% +) are pre-paid now.

6) Myntra and Jabong have spoiled me with their super easy return/exchange policies and flow. I don’t think twice before ordering stuff from them as I know I can always get the product returned/exchanged if I don’t like it. They also have superb delivery timelines (24 hours is a regular)

7) One thing I miss shopping online, is “Lack of Price Protection”. What you buy today for Rs 5000 can be available for say Rs 4000 and Rs 3500 the next day. As a buyer, you obviously feel bad about it

8) Newly caught trend of using wallets to pay on various sites to get discounts and cashbacks is a good incentive to use them. I’ve used Paytm, mobikwik and Payumoney, depending on the offers they are running.

9) I’m yet to order specs, furniture, grocery, health & wellness and things from a lot of these categories

10) Product wise – Wishlist and Rating/Reviews are by far the most useful features. Also, I love the feature to sort/filter using discount/offers (or the lack of them).

Hope, this post would help folks working in e-commerce get “some more idea” of their *Customers*

Despite all the jig bang the Indian cyber space has kinda been hostile to the incumbents of online dating ecosystem. Dating as a concept is yet to catch up here but some of the newly launched mobile apps seemed determined to change that.

Thrill, is one such new dating app on the block ( H/T @pacificleo). Android based and targeted for Indian users.

Founded in Nov 2012 in Singapore by Josh Israel and Devin Serago. The USP of the app is that on Thrill, women have the absolute power to decide which guys to accept and reject.”He applies. She decides” goes the tagline

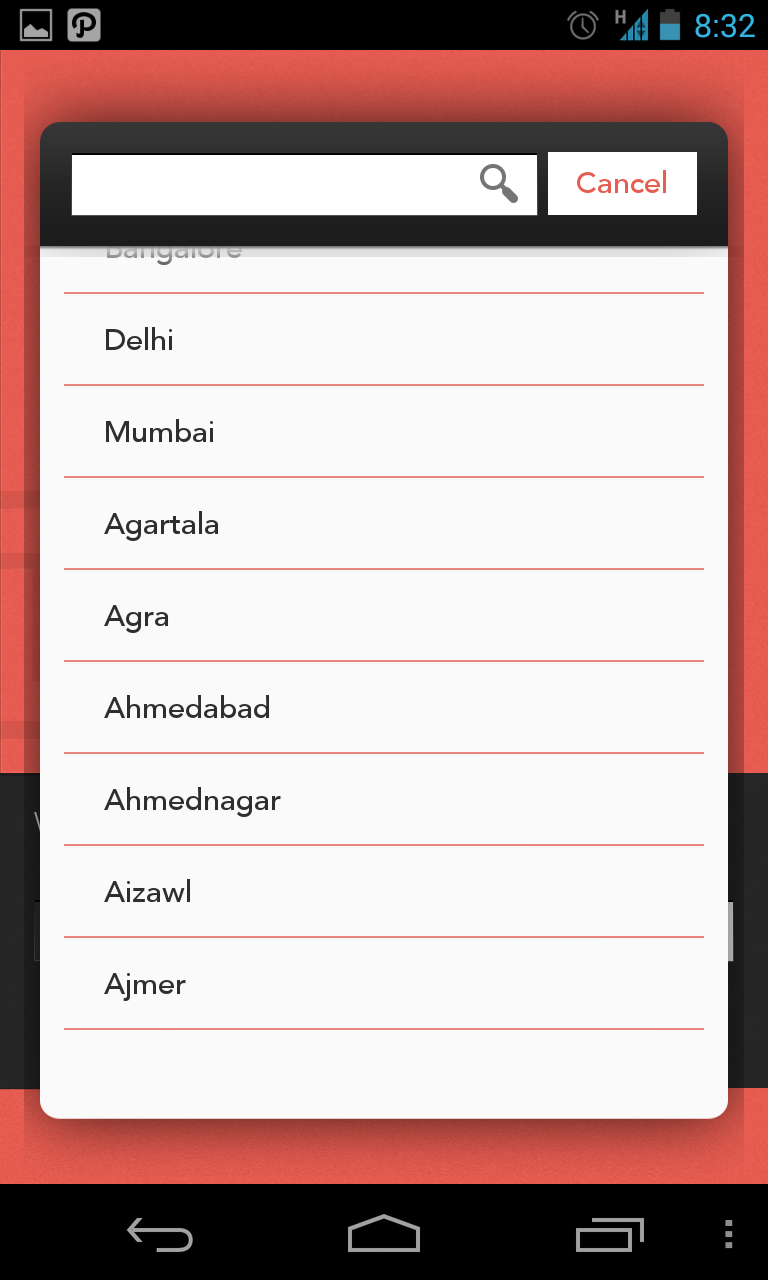

The metros figure up on top of the list followed by other cities arranged alphabetically. Good thing

3) Apply & Wait

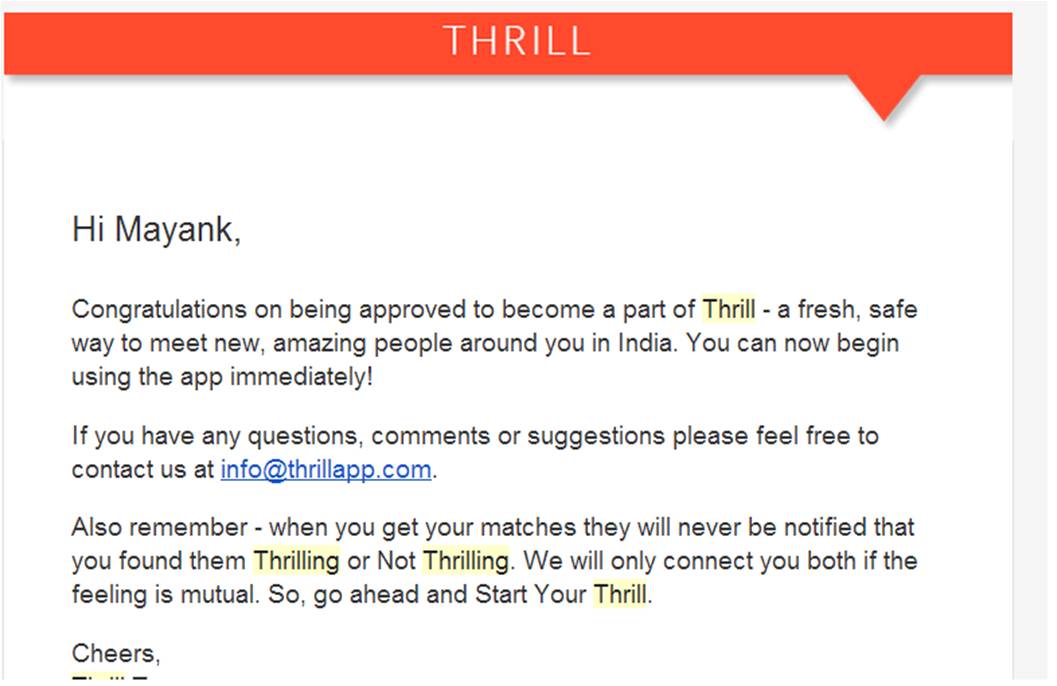

Thrill isn’t an open platform (at least it wasn’t when I used it for the first time last month). You apparently are placed in a queue to verify your profile and make it look exclusive. A social share in hopes of moving up the queue is a bonus. I didn’t share socially but got an approval in a day or so

We will only connect you both if the feeling is mutual

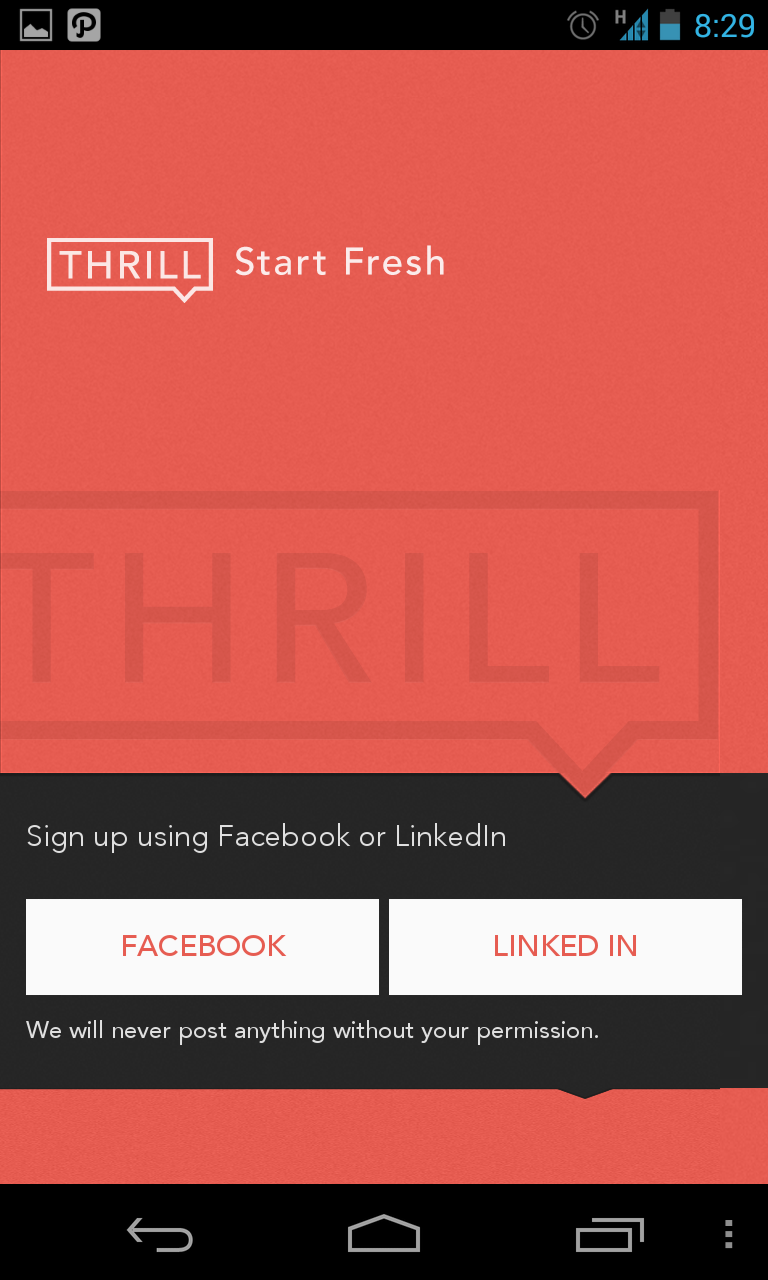

4) Gender Selection, Sign up and Social profile Access

a)

b)

c)

Three screens to select gender, choose sign up via social profile and then grant access is an overkill.

Possible Alternatives:

Show screen 4b) first and add profile access disclaimer there itself. Ask for gender only if the user hasn’t filled in their gender in their profile.

Also, WHO/WHY would anybody sign in with their Linkedin Profile on a dating app? I’d be really interested in knowing what % of signups happen through linkedin. (Use Twitter or Google instead)

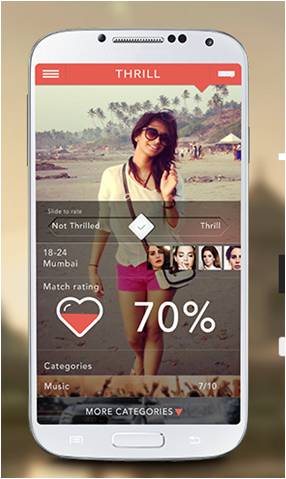

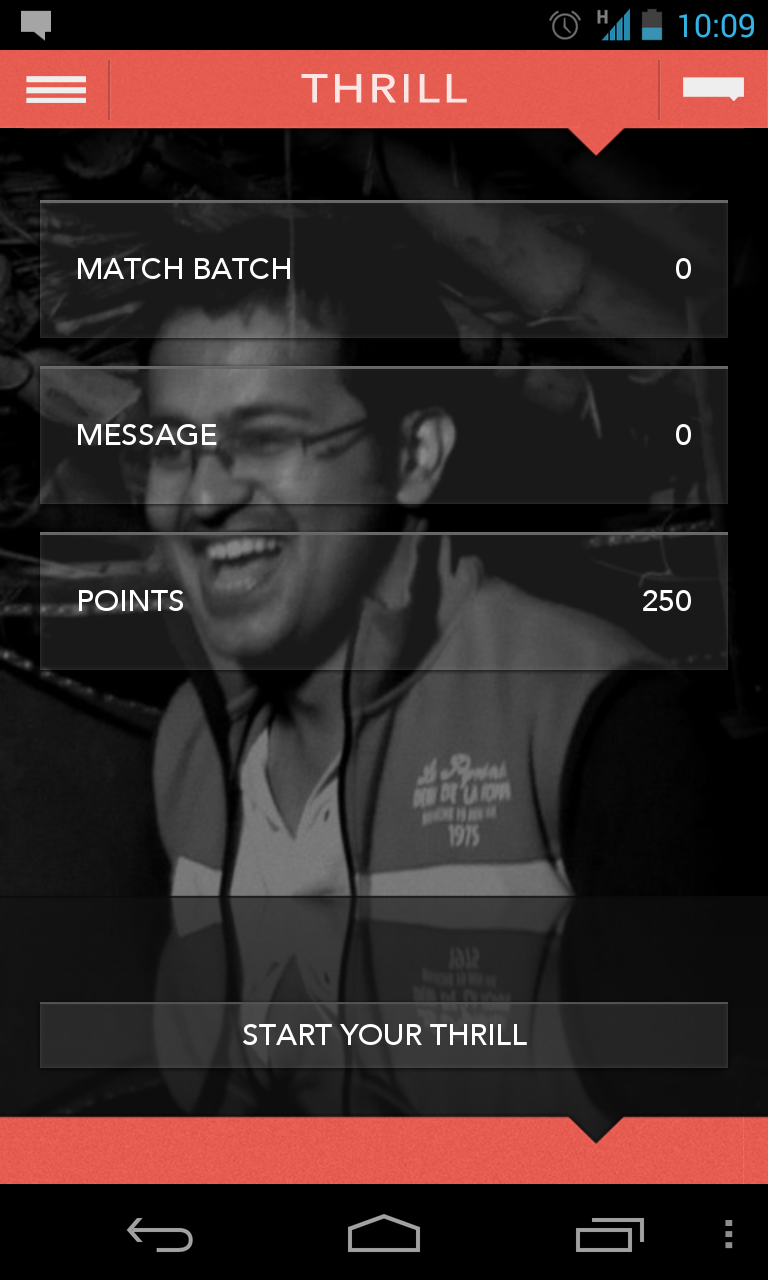

5) Dashboard

Comments: As a first time user, I have no clue what a “Match Batch” is and what’s the deal with “Points”. Anyways, I’d click “Start Your Thrill” as the call to action is quite powerful.

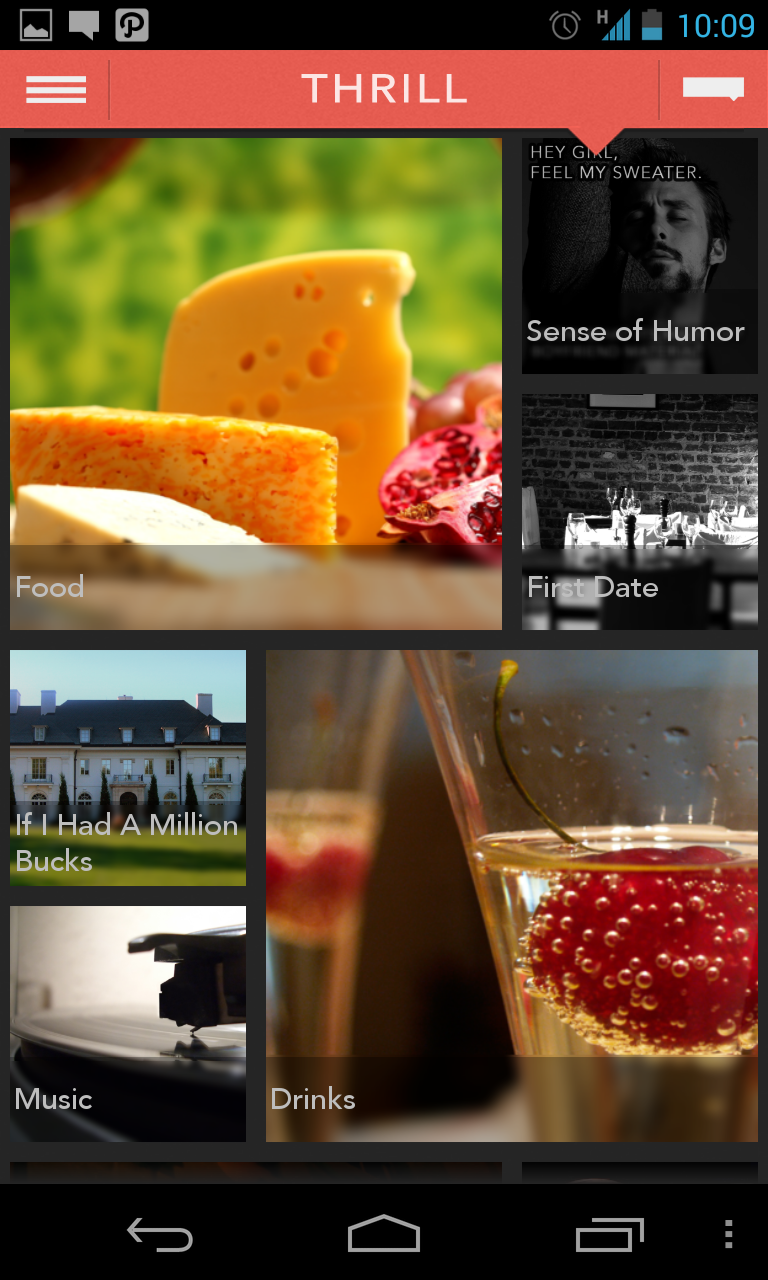

6) Starting Thrill

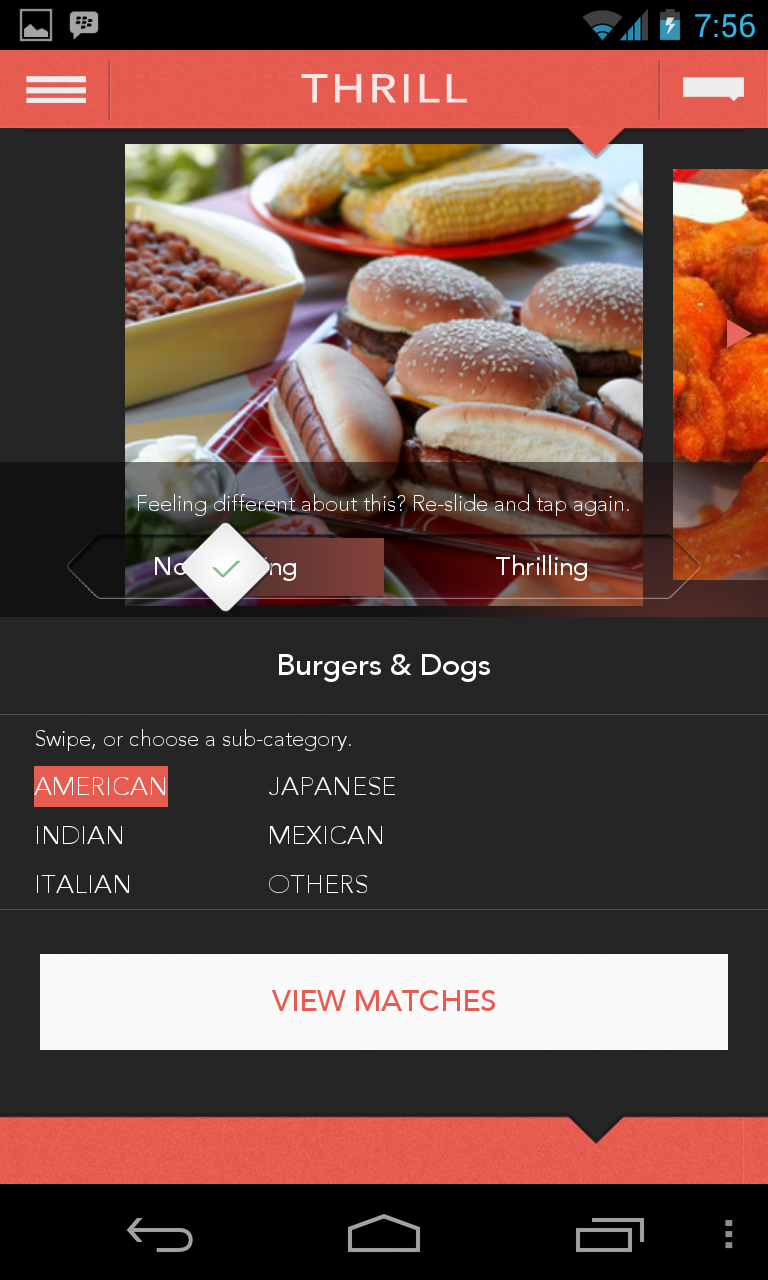

a) Select Category

Comments: This screen isn’t that intuitive, some overlays would help a newbie figure out how to go ahead.

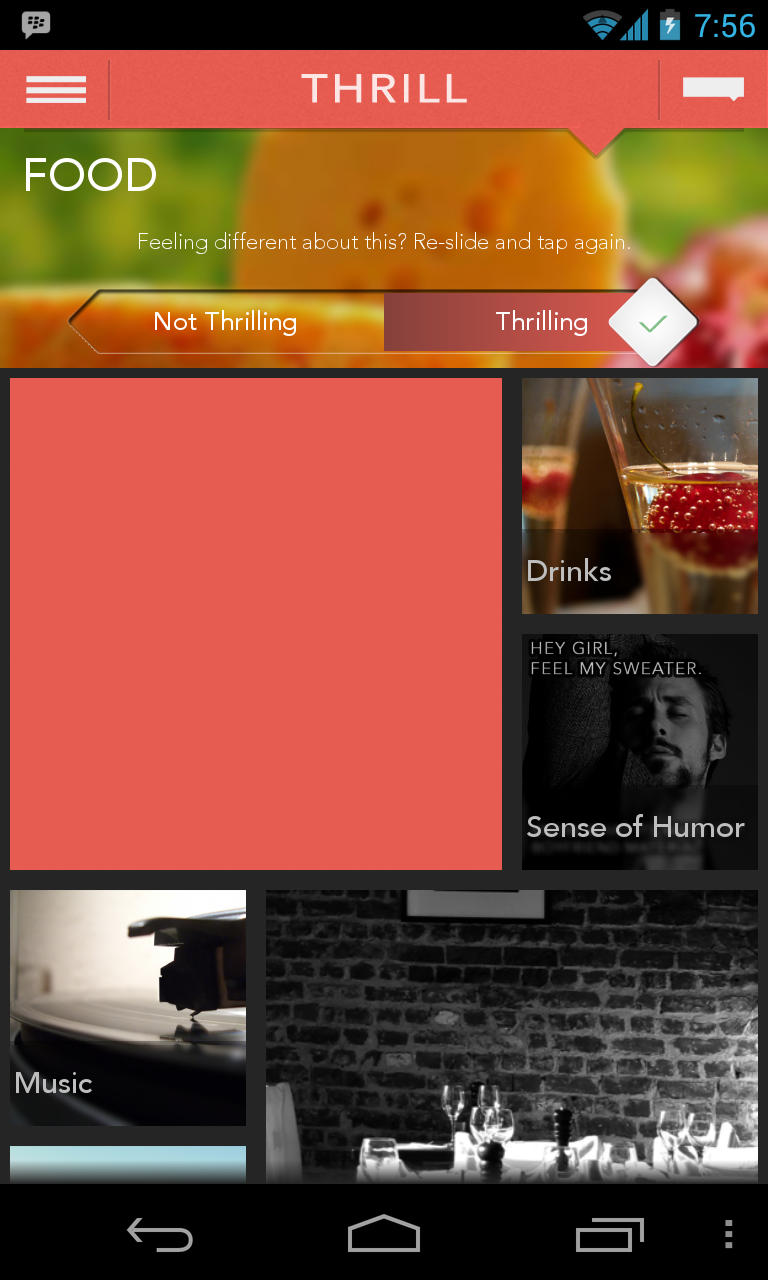

b) Rate Category

Rating a category bit didn’t seem needed and also added an unnecessary extra step in the flow

c) Rate Item

After rating a few items you get an option to view matches.

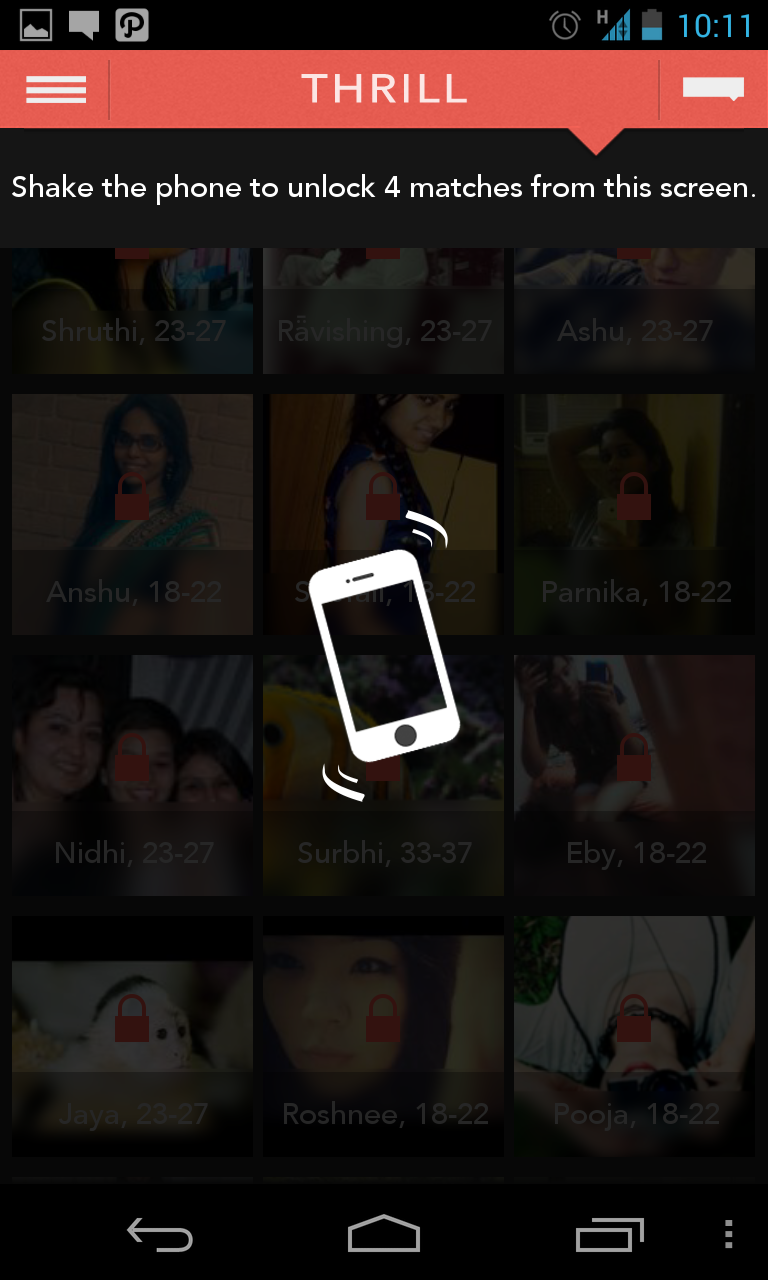

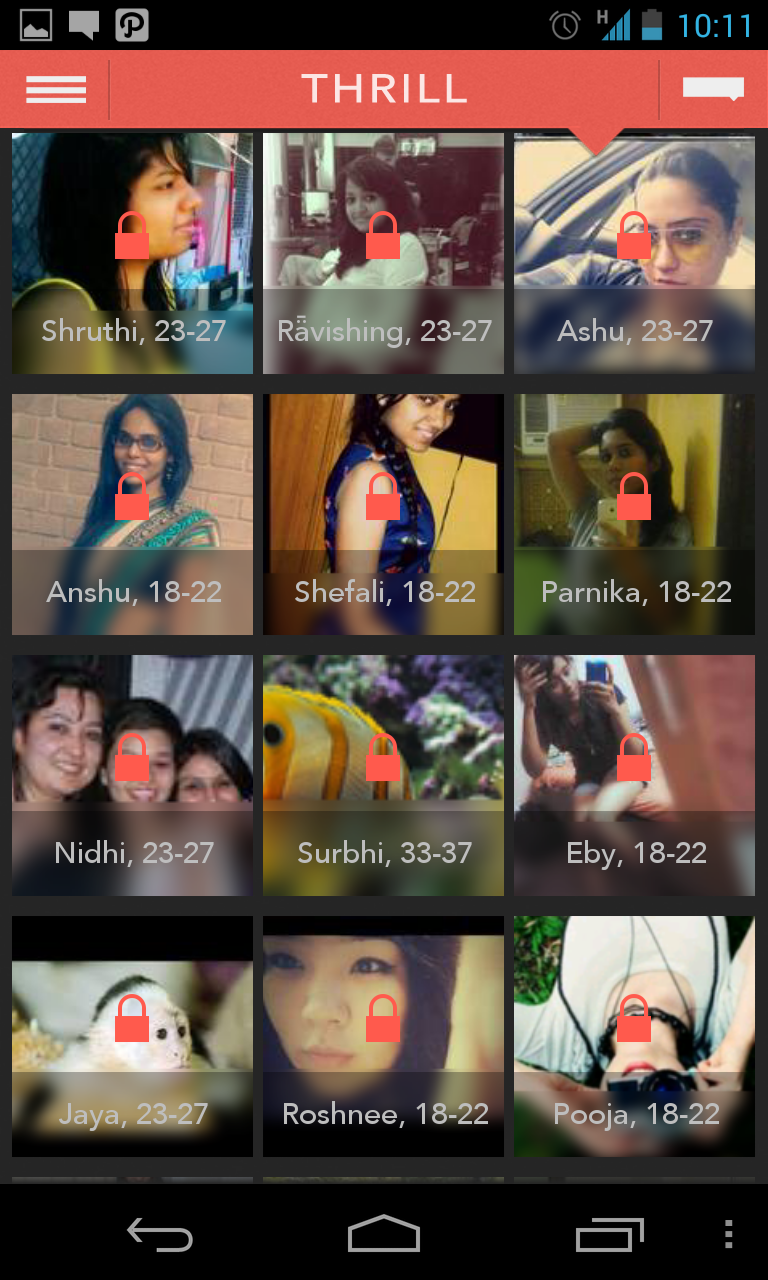

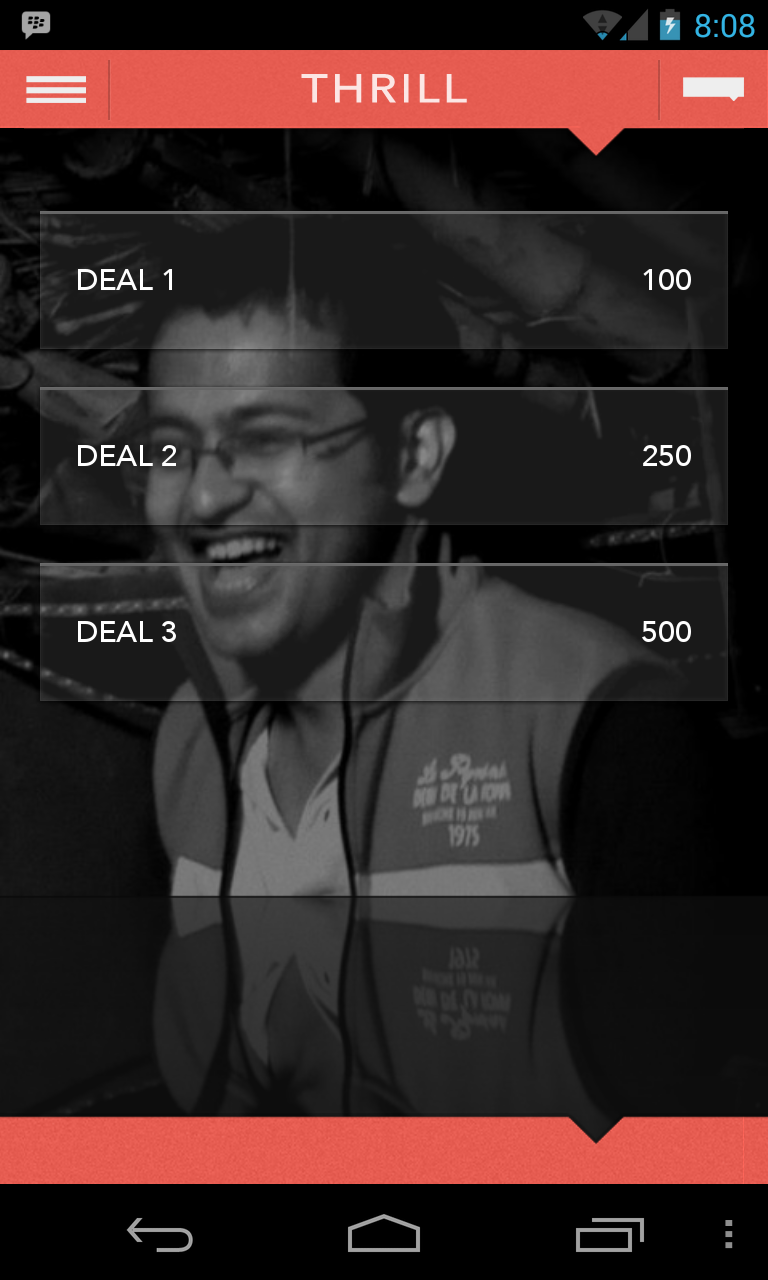

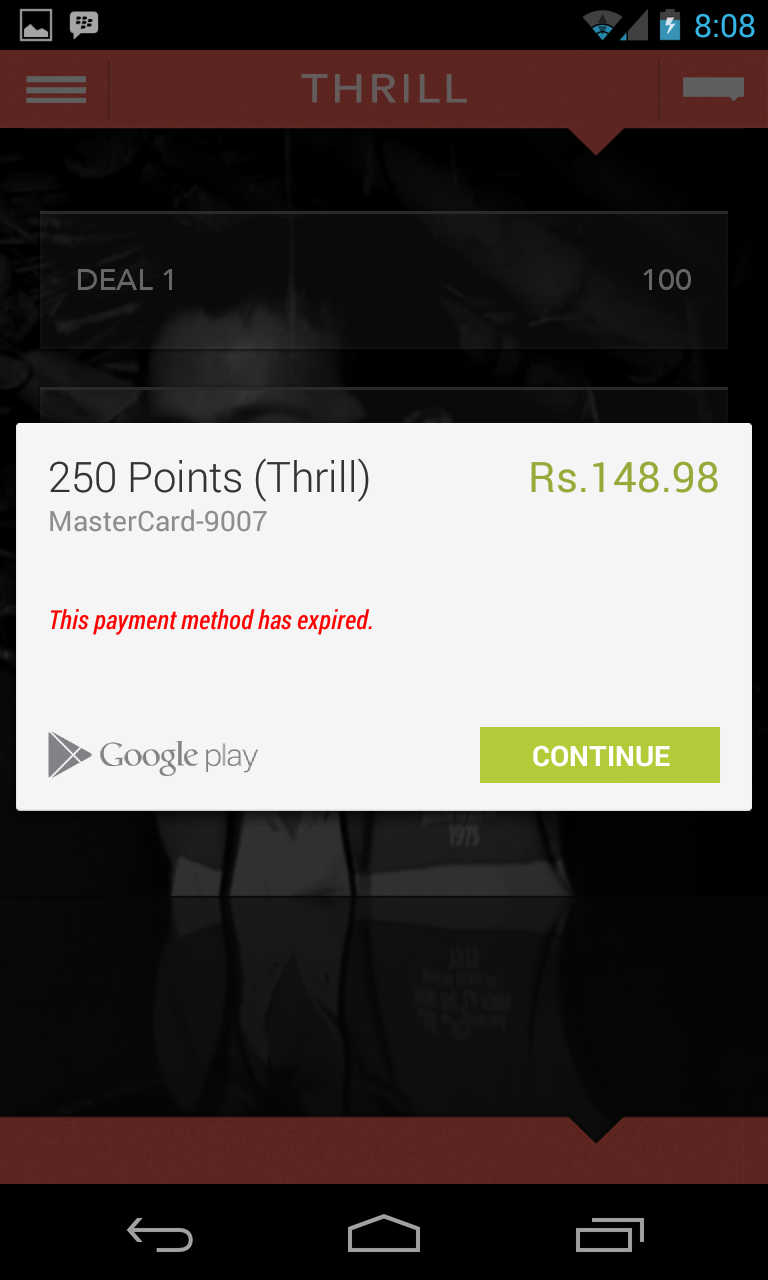

7) See Matches

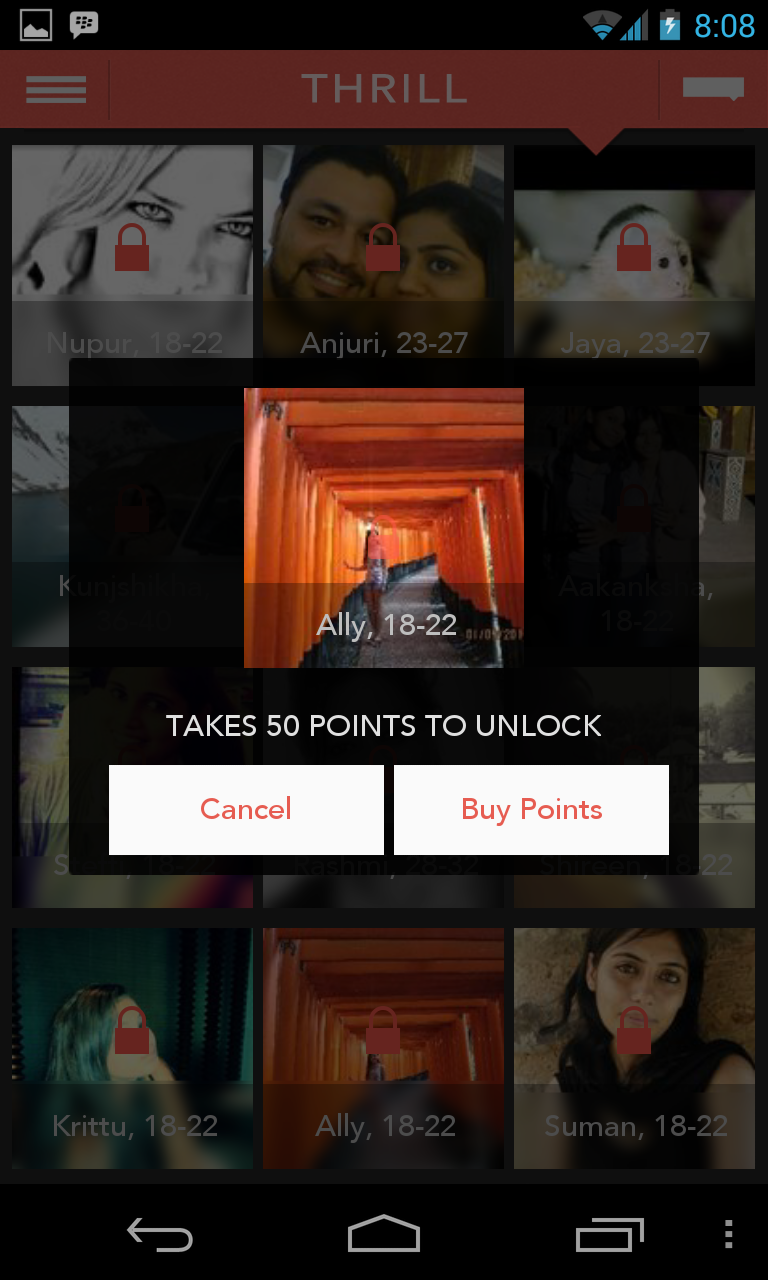

Based on how you rated various items you are presented an unlock batch of matches, you can unlock some of them initially by shaking your phone or eventually by buying credits (Freemium mode #goodone)

This page where the user is supposed to choose how many points do they want to purchase isn’t quite clear. I am not sure if Deal 3 is for 500 points or 500 Rs. Also, some help on how much is 1 point for, and a few basic FAQs in form of a link etc would be of appreciated.

Phew !!

Overall the app seems to be very neatly designed(UI and UX), is fairly fast and has an interesting take on dating. The concept of rating various categories and items in them to be able to find a matching profile is fairly intuitive.

Initially it had some bugs (app freezing or crashing during certain events) which were fixed in subsequent updates.

I haven’t used dating apps so don’t really know what the ideal/expected scenario is. Do users keep using the app actively or they find a match or two and leave?

Apart from the extended workflows required for certain actions I am apprehensive on how would they solve the

Should the part of rating be one time during on-boarding or a regular affair? For example if have I rated all food items, is it done or after some time there will be new items which I’d be required to rate to be able to find new set of matches? Perhaps the core experience could be made simpler and an easy win given to the user

Chicken and Egg problem : Despite giving the app a spin for a few weeks, the overall user base didn’t seem to be increasing much. There is no way to know if more and more women are joining the app. I think unless this is the case or you find a match early one, I am not too sure why would someone keep coming back to the app.

Customer On boarding- 3/5

Engagement -2/5

Look and Feel – 4/5

For the sake of exploring, I signed up to snapdeal.com. Since the intention was to explore the website and not to buy, I went straight on to the sign up link and here’s how it worked after that

Step 1: Click ‘My Account’ Link

Since this is the only link on the menu (no login/signup etc), I clicked it and was presented with the following

Did you see the top most tabs of login and signup? Neither did I. Since I am not quite comfortable signing up with Social Logins I chose to create an account. This page is as far from a neat/uncluttered page as possible and who the hell signs up using “Yahoo” anyways?

Step 2: Click the ‘Create your Account Now’ link

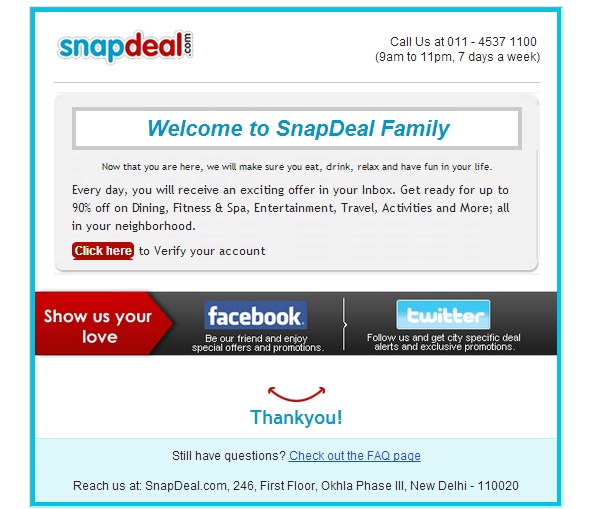

After filling up the form, I was sent a confirmation email. Here’s how it looks

Oh wait, did the email say ?

Now that you are here, we will make sure you eat, drink, relax and have fun in your life.

Every day, you will receive an exciting offer in your Inbox. Get ready for up to 90% off on Dining, Fitness & Spa, Entertainment, Travel, Activities and More; all in your neighborhood.”

Looks like in all the jazz someone forgot to tell the new users that the core business model has changed from local deals to an e-commerce marketplace

Step 3: Click the verification Link

On clicking, the verification link. It asks me to type my credentials again to login.

Step 4: Login

Not sure why on earth is Snapdeal making me do all this work just to sign up ?

Let’s compare this with let’s say Flipkart’s signup workflow

Step 1: Click ‘Signup’ link

Unlike Snapdeal which assumes every user has an account on their website and wants to immediately jump to it, Flipkart’s menu has the following links ‘Login | Signup’. As explicit as it can get

Clicking Signup link opens the following

Much neater and usable none the less

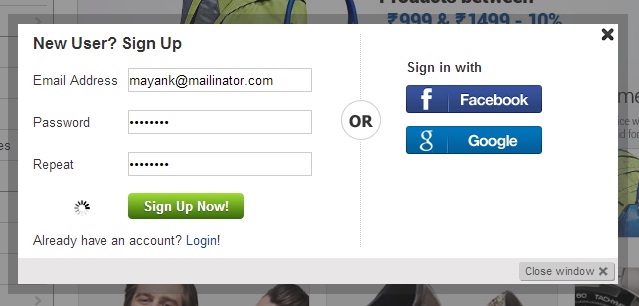

Step 2: Enter details and click Sign up Now!

After filling the details and clicking Sign up Now!, I don’t need to a) click verification email b) login on the website

Voila !! All of this is taken care of by itself

I hope now even a rookie can now appreciate how bad Snapdeal’s workflow is